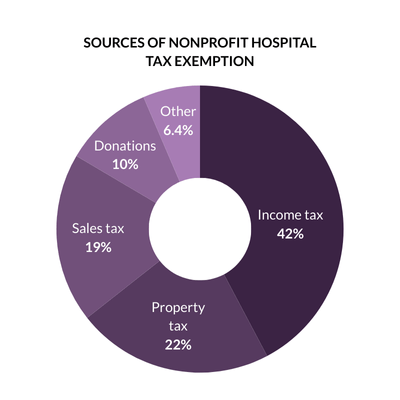

Overall, hospitals in 20 states collectively received $26 billion per year in tax breaks.

Income tax (42%) – The value of the federal income tax made up the largest proportion of the tax exemption for hospitals in these 20 states (32% of the total) at $8.3 billion. The value of the state income tax made up 10% of the total tax exemption, at $2.7 billion. Two states (OH, TX) do not have a state corporate income tax.  Six hospitals in our data set made at least $1 billion in a year from 2020-2022, according to CMS cost reports. One hospital (the Mayo Clinic in Rochester) reported making at least $1 billion in two of the three years.

Six hospitals in our data set made at least $1 billion in a year from 2020-2022, according to CMS cost reports. One hospital (the Mayo Clinic in Rochester) reported making at least $1 billion in two of the three years.

Property tax (22%) – Property tax made up 22% of the tax exemption value for hospitals in these states, totaling about $5.8 billion. This value was concentrated among larger hospitals in major cities such as New York City, Boston, Orlando, Cleveland, and San Francisco. The 20 hospitals with the largest real estate property tax exemptions avoided nearly $1 billion in property taxes collectively.

State and local sales tax (19%) – State and local sales tax made up 19% of the total for hospitals in these states, totaling about $4.8 billion. Four states (CA, OR, LA, NC) did not exempt hospitals from sales taxes. In New York, sales taxes made up the largest portion of the tax exemption due to higher spending on supplies and high sales tax rates.

Tax-exempt donations (10%) – The value of tax-exempt donations made up 10% of the total at $2.7 billion. Five hospitals in our data set received at least $50 million in tax-exempt donations. Donations were reported on IRS Form 990, excluding government grants and in-kind donations.

Other tax benefits (6.4%) – Nonprofit hospitals benefit from being able to issue tax-exempt bonds because they can offer a lower interest rate to investors. The value of tax exempt bonds made up 6% of the total tax exemption, totaling $1.7 billion per year on average. Hospitals are exempt from paying federal unemployment tax as a result of their nonprofit status. The federal unemployment tax exemption made up 0.4% of the total tax exemption at $106 million per year on average. This element of the tax exemption is relatively low, because we assume that hospitals paid state unemployment taxes and took the full exemption from the maximum federal unemployment tax exemption rate.

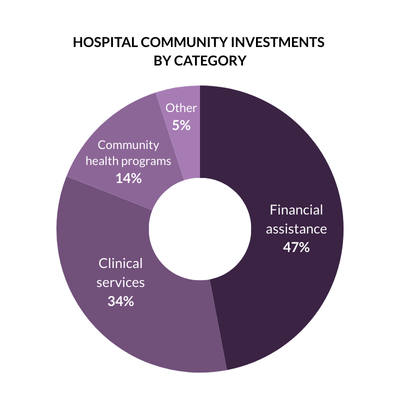

Overall, hospitals in 20 states gave $22.4 million per year in community investment.

Financial assistance (47%) – The largest proportion of community investment was spent on financial assistance (free and discounted care for eligible low-income patients), with hospitals spending $10.6 billion on this category.

Notably, in Texas, Tennessee, and North Carolina, at least 75% of total community investment went to financial assistance, which suggests that the need for financial assistance (due to not expanding Medicaid) is crowding out hospitals’ efforts to invest in health upstream.

Notably, in Texas, Tennessee, and North Carolina, at least 75% of total community investment went to financial assistance, which suggests that the need for financial assistance (due to not expanding Medicaid) is crowding out hospitals’ efforts to invest in health upstream.

Clinical services (34%) – Subsidized health services (clinical services that meet an identified community need, provided at a loss to the hospital) was the second-highest spending category, with $7.7B. These included service lines such as substance use treatment, rural health clinics, and behavioral health services. Despite these services making up the largest portion of community investment in many states, some hospitals provided limited details on the service lines to which this spending was attributed.

Community health programs & social determinants of health (14%) – Despite hospitals and public health experts putting increased emphasis on social drivers of health in recent years, relatively little spending went to community health improvement or community building activities. Together, these categories represented 14% of total community investment, around $3 billion in spending per year.

CHICAGO TRIBUNE

AXIOS

CRAIN’S CHICAGO

CRAIN’S NEW YORK

CRAIN’S GRAND RAPIDS

NPR TAMPA (WUSF)

IDEASTREAM PUBLIC MEDIA

DENVER BUSINESS JOURNAL

BECKER’S HOSPITAL REVIEW

THE JOURNAL GAZETTE

CLEVELAND.COM